Before and after

7 May 2025- April’s tariff chaos gives way to nervous calm

- Trade war impacts on NZ still unclear, but high chance we pull back our 2026 growth forecasts

- We still see enough economic supports to sustain forward momentum this year

- No change to our cash rate and mortgage rate views. We run a fix-or-wait scenario to tease out some of the risks.

The chaos of early April has given way to a nervous calm in global financial markets. Some signs of de-escalation in the trade war have helped. But it still feels like we’re traversing a ‘before and after’ moment for the global economy.

Some of the global activity numbers we’re watching have turned down, but most are yet to fully capture the impact of trade disruptions. It’s likely things will deteriorate further, but it’s all a bit of a guess as to how much.

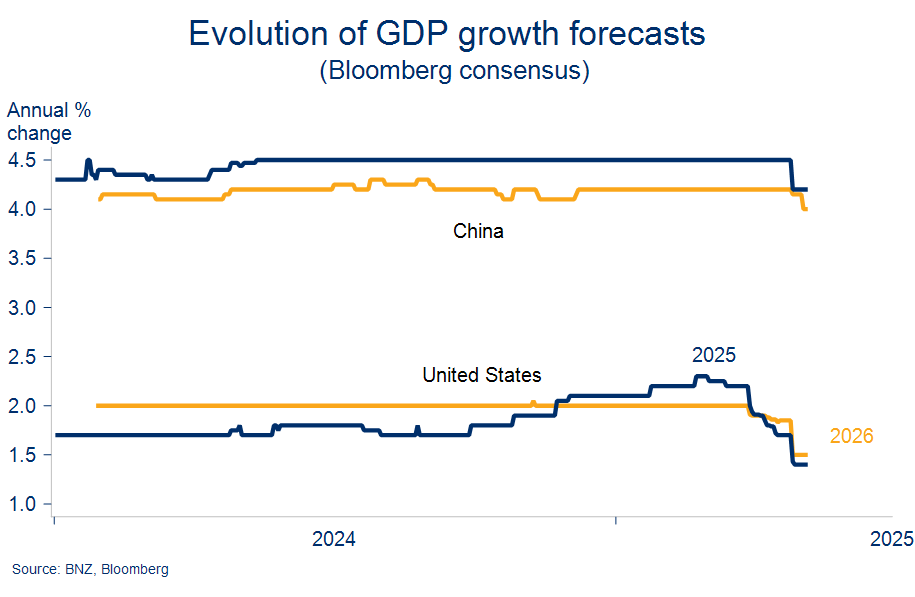

Interesting but perhaps unsurprising is the fact that forecasters have taken more of a gouge out of US growth prospects than many other countries. In the space of a month, almost a full percentage point has been lopped off the consensus US growth forecast for 2025 (now 1.4% y/y). Surveyed odds of an outright recession have climbed to 40%. We learned last week that the US economy is half-way there already with GDP contracting in Q1.

The consensus has not been as harsh on China’s growth prospects. GDP forecasts have so far been nudged down only a few tenths to 4.2% for calendar 2025. Exports to the US are a large part of the Chinese economy (about 3%). But the prevailing view is that China has a greater ability to cushion the trade blow with monetary and fiscal stimulus, and perhaps some trade diversion.

A big trade skirmish between the world’s two largest economies (43% of global GDP combined) will have a chilling impact on global economic growth. Estimates of such are starting to surface but should be considered works in progress given still near-daily changes in US trade policy.

Not only do we not know where tariff rates will end up, there’s also the ‘known unknown’ of how affected countries ultimately respond (for example with fiscal policy), and how much of a cushion this and some trade diversion might provide.

Some prominent organisations have given up forecasting altogether. But, as a starter for ten, NAB economists have lowered 2025 global growth forecasts to 2.7%, a marked slowdown from last year’s 3.3%y/y. That doesn’t sound overly dramatic, but would still amount to the slowest growth (ex-COVID) since the 2008/09 global financial crisis.

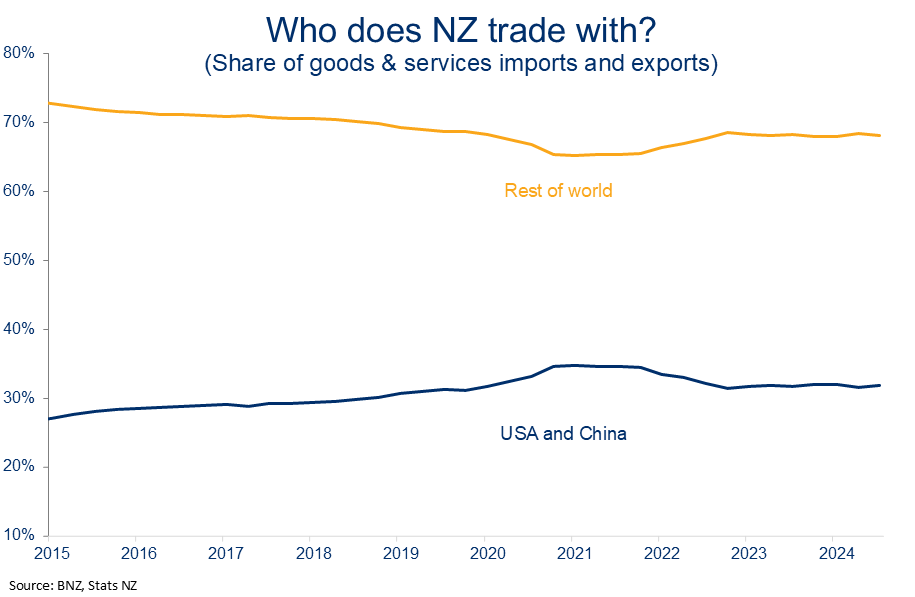

With things still moving we’ve resisted the urge to distil this into a precise impact on NZ’s economy. But NZ is clearly exposed to a slowing in global growth. Just over a third of all NZ trade (goods and services imports and exports) takes place with China and the US.

We suspect the most immediate impact on NZ’s economy will be via heightened uncertainty. This effect is now clearly on show in the US but in our recent travels have also picked up anecdote of some investment or expansion projects being, if not cancelled, then paused. There was evidence of this in last week’s ANZ’s business survey. Firm’s investment plans were rowed back aggressively over the second half of April. It’s hard to know how much of this will be sustained. But for a business community already gun-shy, the skittish global backdrop is simply another factor likely to delay the turning of the investment cycle.

Combined, the trade and investment impacts of the trade war are likely test the sustainability of NZ’s economic recovery. We see this as more as a risk to next year’s growth outlook, with the 2.7% annual GDP expansion in our forecasts now at serious risk of a downgrade.

For this year, we still see enough economic support in the wings to sustain forward momentum. It’s go-forward, but not the kind to set pulses racing, with an average run-rate of around 0.5% GDP growth per quarter pegged for calendar 2025. Important supports include:

- The dairy and primary sector cash that is now flowing strongly. We’re watching things closely, but are yet to see any noticeable impacts on elevated commodity export prices from the recent trade turbulence. Both GDT dairy auction prices and financial market expectations (futures) for Fonterra’s current season Milk Price have nudged upwards in recent weeks. The latter is now at $9.90 kg/ms in the wake of this morning’s positive GDT result.

- The low NZ dollar will further assist exporter returns. At around 0.6000, the NZD/USD is 6-7 cents below the 10-year average. Admittedly, the low currency may not stick around at these low levels for long. Our long-held view of NZD/USD appreciation was pulled forward last week such that our year-end guidance has been upgraded to 0.6500. It’s mostly a story of the US dollar being further undermined this year.

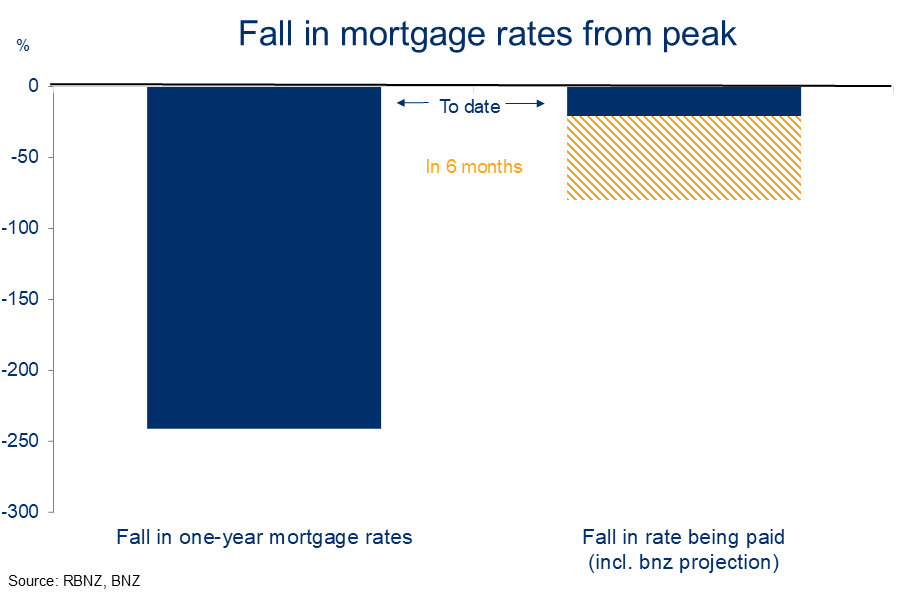

- The delayed gratification of lower mortgage rates. The majority of positive cash flow from falling mortgage rates is yet to filter through, but will do so over the coming 6-12 months. The example in the chart illustrates the point. Carded one-year fixed mortgage rates are now about 2.4 percentage points below the peak but the average rate being paid by borrowers (as at February) is only 0.2 percentage points below the peak. Our estimates have this average paid rate falling to around 5.6% in six months’ time, as borrowers re-fix onto lower rates. That’s a cash flow of roughly $2.2b going back into mortgage-holders’ pockets.

A good chunk of the extra cash may well go on paying the bills. But it should at least steady the unsteady recovery in retail spending seen since August. Elevated costs and a still-weak labour market will keep working in the other direction.

Despite these supports, we remain of the view the fledgling recovery is going to need a little more help. And, as the finance minister made clear again last week, there’s not a lot of room for additional fiscal support. So it’s going to be the Reserve Bank and interest rates doing the work in the first instance.

Uncertainty naturally increases the range of potential outcomes for interest rates. Hence the wider dispersion and more frequent changes to some of the interest rate forecasts out in the market. On our reckoning, our central view still treads a path somewhere through the middle of the many risks shrouding the outlook. So we haven’t changed it. The guts of that view being:

- Three further 25bps cuts in the Reserve Bank’s Official Cash Rate (OCR), taking it to a low point of 2.75% by August. Market pricing has moved such that it largely enshrines this view, meaning market interest rates could rise in the event additional cuts are not delivered. We doubt the RBNZ would view that as desirable at this point.

- Should these cuts transpire, short-term mortgage rates have a little further to fall. Our best guess is still that six-month and 1-year fixed mortgage rates dip into a 4.7-5.0% range over the remainder of the year. There’s less downside on longer-terms (two years plus) with the bulk of the downtrend in those rates likely behind us.

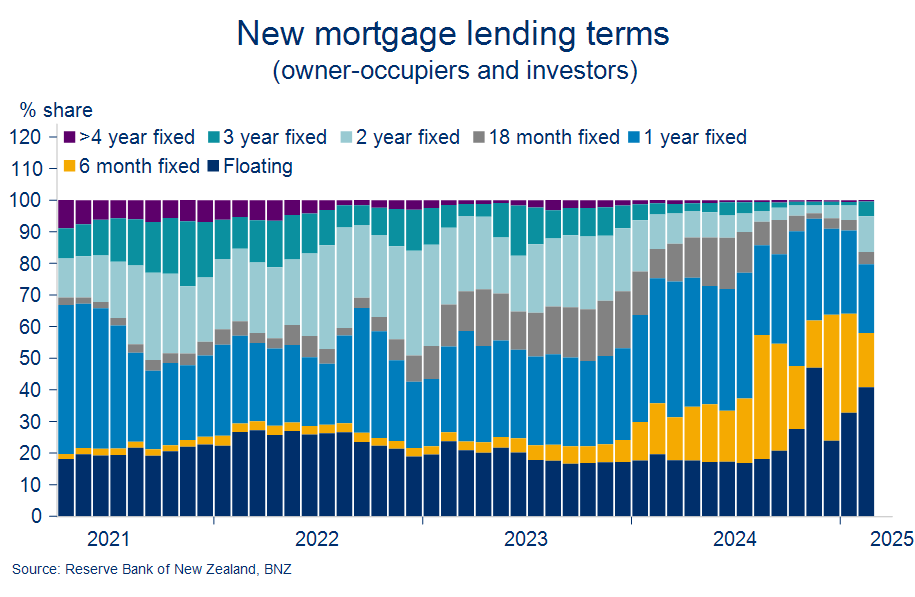

- On the basis of the above, the economics of floating, or fixing for very short-terms, still looks stretched. That is, we haven’t changed the view expressed most recently here. Borrowers have started to dip their toes into longer fixed terms with, for example, the share of lending at 2-year fixed terms in February the highest in a year (chart below). Floating nevertheless remains a popular choice as some opt to pay the higher associated upfront costs on hopes term rates fall a little further in coming months.

That’s not unreasonable as there is potential for some rates to fall a little further given the risks to the outlook. However, this potential opportunity needs to be balanced against the cost of waiting to term out debt.

For example, there’s currently a 1.7 percentage point difference between carded floating mortgage rates and the 4.99% 2-year fixed rate[1]. On a hypothetical $200k tranche of borrowing that equates to a $283/month relative cost to float. Expressed another way, at current rates, the 2-year fixed rate needs to fall 0.07 percentage points per month for the borrower to ‘break-even’ on the extra cost of remaining floating. A four month wait on floating rates would thus entail an upfront cost relative to fixing for 2-years of just over $900 (assuming no change in 2-year rates and making some allowance for forecast cuts in OCR/floating rates), or a required fall in the 2-year rate to about 4.75% over those four months to break-even.

For some that will be a risk worth taking but we suspect many will opt to take the additional certainty and upfront cash flow benefits of longer-term fixed rates. Getting the mortgage strategy “right” of course ultimately depends on individual borrower’s financial needs and requirements for certainty.

It also bears repeating that all of the above is subject to significant uncertainty given the unpredictable offshore picture. Things are changing rapidly so take all views and forecasts with a grain of salt!

[1] All rates quoted are an average of the four major banks and sourced from interest.co.nz.

To subscribe to Mike’s updates click here

Disclaimer: This publication has been produced by Bank of New Zealand (BNZ). This publication accurately reflects the personal views of the author about the subject matters discussed, and is based upon sources reasonably believed to be reliable and accurate. The views of the author do not necessarily reflect the views of BNZ. No part of the compensation of the author was, is, or will be, directly or indirectly, related to any specific recommendations or views expressed. The information in this publication is solely for information purposes and is not intended to be financial advice. If you need help, please contact BNZ or your financial adviser. Any statements as to past performance do not represent future performance, and no statements as to future matters are guaranteed to be accurate or reliable. To the maximum extent permissible by law, neither BNZ nor any person involved in this publication accepts any liability for any loss or damage whatsoever which may directly or indirectly result from any, opinion, information, representation or omission, whether negligent or otherwise, contained in this publication.